Africa’s travel ecosystem is entering a decisive growth phase. According to the International Air Transport Association (IATA), African airlines have recorded sustained passenger demand growth in recent reporting periods, reflecting the continued recovery of international travel and strengthening regional mobility. At the same time, the UN World Tourism Organization (UNWTO) highlights Africa as one of the fastest-rebounding tourism regions globally, supported by rising leisure, diaspora, and business travel flows.

This growth is increasingly digital. Online travel agencies (OTAs), airline apps, and booking platforms are capturing a larger share of travel transactions as smartphone penetration deepens across African markets. Research from Statista shows that online travel sales across Africa continue to expand year over year, with mobile bookings playing a central role in customer acquisition and conversion.

Yet beneath this momentum lies a structural constraint: payments. Airlines and OTAs serving African customers frequently encounter higher transaction failure rates, currency complexity, and settlement friction, particularly in cross-border payment scenarios.

This SeerBit article explores why cross-border payments remain one of the most critical and underestimated challenges in Africa’s travel economy, where airlines and OTAs lose revenue, and how modern travel payments infrastructure can unlock higher conversion rates, smoother settlements, and stronger customer trust.

Why Cross-Border Payments Are Uniquely Challenging in Africa

Multiple currencies and FX complexity: Africa is not a single payments market but a network of diverse currencies, monetary policies, and foreign exchange realities. Airlines pricing tickets in USD or EUR often serve customers earning and paying in NGN, KES, GHS, ZAR, and many other currencies. Each conversion introduces FX spreads, volatility exposure, and potential pricing perception challenges.

For travellers, unexpected currency conversions or unclear FX charges create friction at checkout. For airlines and OTAs, FX inefficiencies affect margins, complicate reconciliation, and introduce forecasting uncertainty. Multi-currency payment capabilities are therefore essential for protecting revenue integrity and delivering transparent customer experiences.

Diverse local payment preferences: Payment behaviour across Africa varies significantly by country, demographic, and access to financial services. While card payments dominate in some segments, many travellers prefer bank transfers, mobile money, digital wallets, or USSD-based payments. A checkout flow built primarily around international cards risks excluding willing customers.

This diversity directly impacts conversion rates. Industry studies from McKinsey and Worldpay consistently show that offering locally preferred payment methods improves checkout completion, particularly in emerging markets. When travellers encounter familiar payment options, trust increases and abandonment declines, especially for high-value purchases such as flights.

Inconsistent card penetration and authorisation behaviour: Even where cards are widely used, approval rates can vary. Issuer risk controls, cross-border transaction restrictions, fraud scoring models, and routing inefficiencies contribute to higher decline ratios for African transactions.

For airlines and OTAs, low authorisation rates translate directly into lost bookings. Unlike low-value retail purchases, flight transactions are rarely retried multiple times by customers. A single decline often ends the purchase journey. Optimised airline payment solutions that intelligently route transactions and manage retries can significantly improve approvals and revenue capture.

Regulatory and compliance considerations: Cross-border payments across African markets operate within evolving regulatory frameworks. Foreign exchange controls, localisation requirements, AML regulations, and data residency policies differ across jurisdictions. Non-compliance exposes travel businesses to financial penalties, blocked settlements, and reputational risk.

Travel companies, therefore, require travel payments infrastructure designed to navigate regional regulatory nuances while maintaining global interoperability. Compliance-ready payment architecture reduces operational risk and supports smoother expansion across African markets.

Where Airlines and OTAs Lose Revenue

Failed or declined transactions: Payment declines represent one of the most visible and costly leakage points in digital travel. Industry data from Cybersource and Worldpay indicates that false declines, where legitimate customers are rejected, account for billions in lost global e-commerce revenue annually.

In travel, the impact is magnified. A declined flight booking is rarely recovered through retargeting alone. Lost transactions reduce load factors, weaken yield optimisation, and increase customer acquisition costs. Improving authorisation performance is therefore a direct revenue protection strategy for airlines and OTAs.

Slow or unclear payment confirmation: Travel purchases carry significant emotional and financial weight. Customers expect immediate clarity. Was the ticket issued? Did payment succeed? Delayed confirmations or ambiguous status messaging erode confidence.

Uncertainty drives support queries, refund requests, and potential disputes. Fast and reliable confirmation mechanisms, supported by modern OTA payments in Africa, are critical for maintaining customer trust and reducing operational strain.

Checkout abandonment driven by friction: Research from the Baymard Institute shows that global checkout abandonment averages nearly 70 percent, with payment friction among the leading causes. In African markets, where connectivity, trust, and payment compatibility challenges intersect, abandonment risks increase further.

Complex redirects, limited payment options, or repeated failures push travellers toward competitor platforms. Each friction point represents not only a lost booking but also a weakened brand experience.

Limited visibility into cross-border settlements: Settlement opacity complicates finance operations for airlines and OTAs. Delays, fragmented reporting, and inconsistent FX reconciliation increase manual workloads and reduce decision-making clarity for CFOs and revenue leaders.

Unified reporting and centralised reconciliation capabilities within travel payments infrastructure improve cash flow management, reduce errors, and enable more accurate revenue forecasting.

What Effective Cross-Border Payment Infrastructure Looks Like

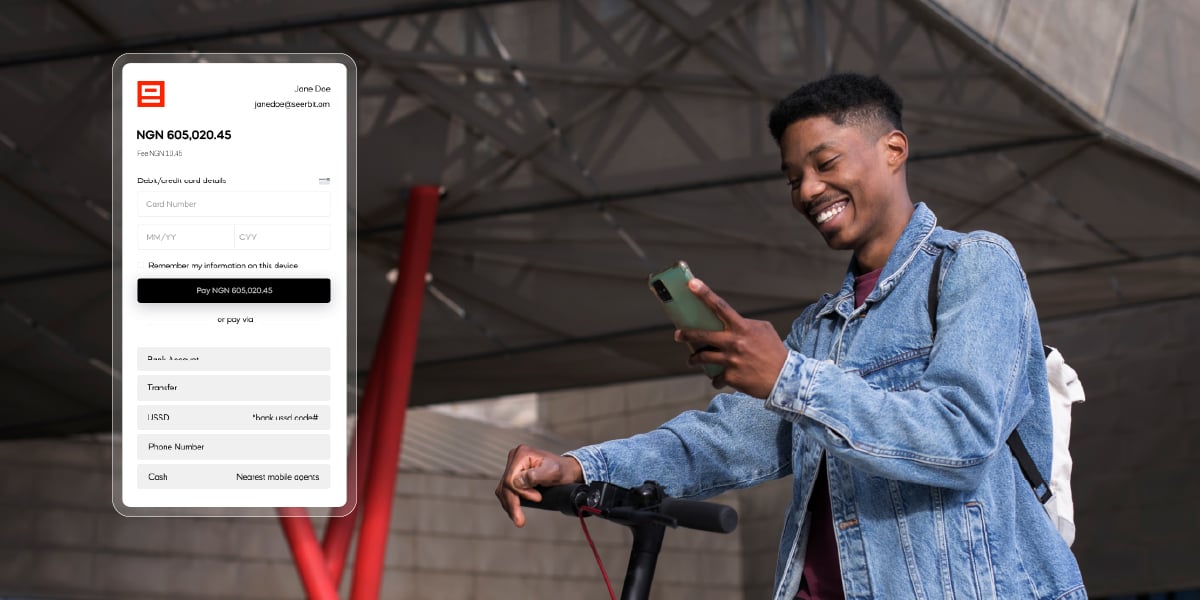

Local payment method support: Supporting regionally relevant payment instruments, including cards, bank transfers, wallets, and mobile money, expands accessible demand. Airlines and OTAs that localise payment options reduce exclusion and align checkout experiences with customer expectations.

Beyond conversion, localisation signals market commitment. Travellers are more likely to trust platforms offering familiar and widely used payment rails.

Multi-currency pricing and settlement: Transparent local currency pricing reduces cognitive friction. Customers can assess affordability without estimating exchange rates, while businesses manage treasury and settlements in preferred currencies.

Effective multi-currency payment strategies balance customer convenience, FX efficiency, and revenue predictability.

High authorisation rates and fast confirmation: Approval performance remains central to digital travel revenue. Intelligent routing, strong local acquiring relationships, and adaptive retry logic significantly influence transaction success.

Fast confirmation closes the psychological loop for travellers, reinforcing confidence and reducing post-purchase anxiety.

Centralised reporting and reconciliation: Travel finance teams manage complex flows that include bookings, cancellations, refunds, and partner payouts. Centralised dashboards that unify cross-border payments data reduce reconciliation overhead, accelerate month-end close, and improve audit readiness.

How Modern Payment Solutions Improve Travel Conversions

Localised checkout experiences: In digital travel, checkout determines whether intent converts into revenue. Even when travellers are ready to pay, unfamiliar flows, foreign currency displays, or unsupported payment methods can trigger hesitation.

Localised checkout experiences reduce friction by aligning payment interfaces with regional expectations. Displaying prices in local currencies and supporting preferred payment methods improves clarity and confidence, ultimately increasing booking completion rates.

Reduced payment friction for cross-border travellers: Cross-border travellers already navigate exchange rates, international pricing, and regulatory differences. Payment failures or repeated authentication steps introduce additional uncertainty at a critical stage.

Reducing friction through intelligent routing, adaptive retry mechanisms, and streamlined authentication flows significantly improves conversion outcomes while reducing customer frustration.

Faster settlement and improved cash flow: Settlement speed directly affects financial performance. Airlines operate within capital-intensive environments, while OTAs manage supplier payouts, commissions, refunds, and treasury exposure. Delayed settlements strain liquidity planning.

Modern travel payments infrastructure accelerates settlement cycles, improving cash flow predictability and working capital efficiency while supporting smoother refund and payout processes.

Stronger customer trust and repeat bookings: Travel purchases are inherently trust-sensitive. Customers commit substantial funds for services delivered later. Failed transactions, delayed confirmations, or refund difficulties erode confidence quickly.

Consistently reliable payment experiences strengthen trust, increase repeat bookings, and enhance customer lifetime value.

Practical Benefits for Airlines and OTAs

Higher booking completion rates: Improved payment performance directly increases booking completion. Higher authorisation success allows airlines and OTAs to capture more value from existing demand without proportional increases in marketing spend.

In a margin-sensitive industry, even modest gains in payment success rates generate substantial revenue uplift.

Reduced operational and finance overhead: Payment inefficiencies generate hidden organisational costs. Failed transactions lead to support escalations, while settlement mismatches increase reconciliation workloads.

Modern airline payment solutions reduce this burden through automation, unified dashboards, and real-time transaction visibility.

Improved visibility into revenue across markets: Cross-border payments introduce FX conversions, fee layers, and settlement timing differences that obscure revenue clarity.

Integrated travel payments infrastructure provides consolidated visibility into transactions, settlements, and FX flows, strengthening forecasting and treasury management.

Scalable infrastructure for peak travel periods: Travel demand is cyclical and event-driven. Festive seasons, promotions, and holiday surges place sudden pressure on payment systems.

Scalable payment architecture ensures stable performance, consistent authorisation rates, and reliable checkout experiences during peak periods.

Key Takeaway for Travel Businesses

Cross-border payments are not merely a backend necessity. They are a core driver of revenue, conversion, and customer experience.

For airlines and OTAs serving African customers, success increasingly depends on payment strategies aligned with local realities, including currency diversity, payment preferences, regulatory requirements, and authorisation performance. Investing in modern cross-border payments capabilities is therefore a growth, trust, and competitiveness decision.

Learn how to simplify cross-border payments for African travel customers. Explore SeerBit’s airline payment solutions and OTA payments in Africa, built for multi-currency payments, high approval rates, and scalable travel payments infrastructure.